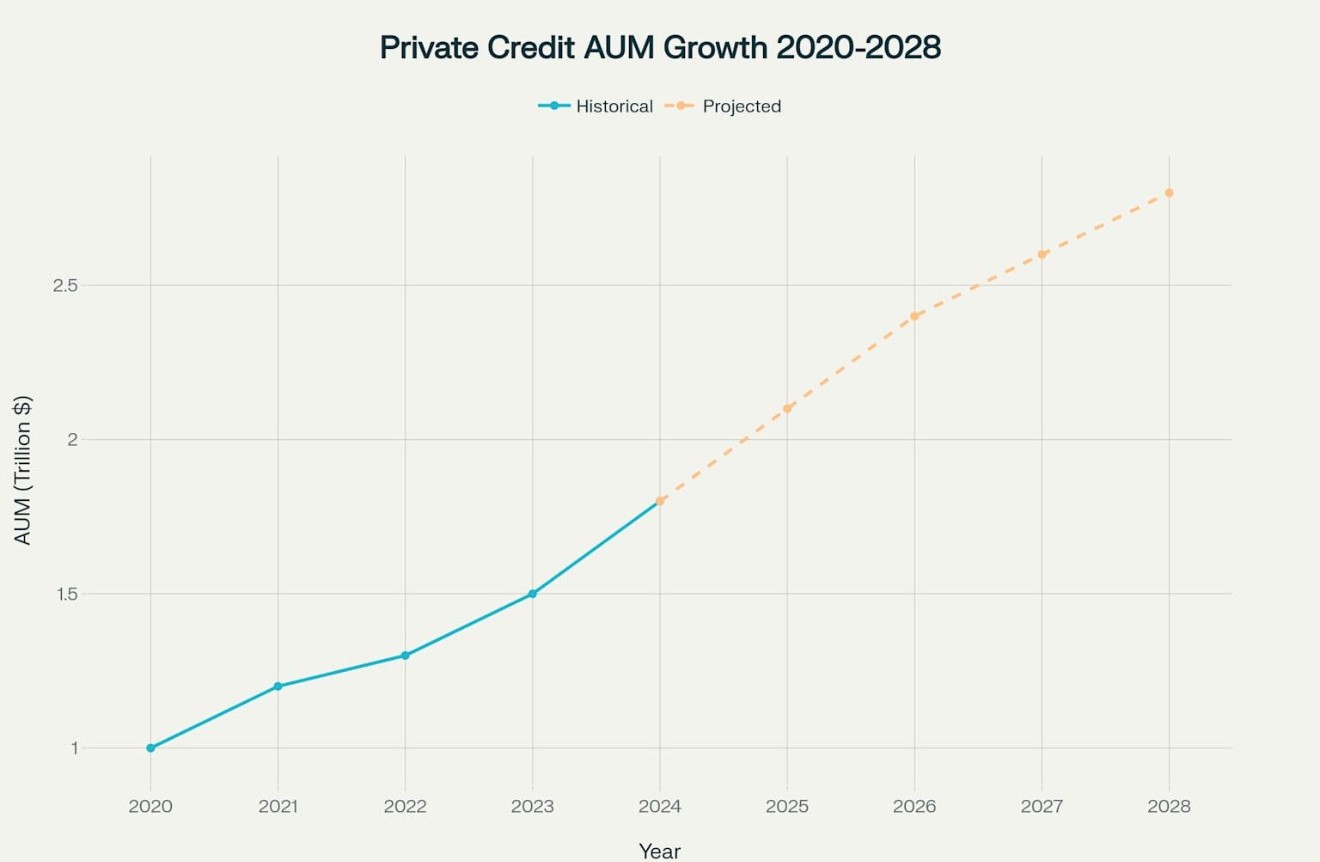

Newsletter

Newsletter 2024 marked a turning point for the direct lending market given the unprecedented number of partnerships forged between banks and private credit providers. The largest transactions are ranging between 12 to 25 billion US-Dollars. These partnerships allow banks to circumvent regulatory capital requirements while still remaining part of the lending market.

They also offer private credit managers crucial deal-sourcing advantages – especially in the non-sponsored segment, which tends to require in-depth relationship management. Both parties bring their own unique strengths to the table. While banks have long-standing client relationships and an established local presence, private credit managers provide the necessary flexibility and capital efficiency for more complex financing structures.

New opportunities in the non-sponsored direct lending segment

The non-sponsored direct lending segment benefits disproportionately from this development as around 90 per cent of all private US and European companies fall under this category. These family-run or owner-managed companies – which have an EBITDA of between 10 and 75 million US dollars – received very little attention in the past because private credit managers traditionally focus on sponsor-backed deals.

As banks already have long-standing relationships with these mid-market companies, the new bank partnerships systematically target them for new business. Non-sponsored deals typically offer a yield pick-up of 100 to 200 basis points compared with sponsored transactions, and allow for stronger covenant structures because there is less competition.

Regional developments in Germany and across Europe

While the German private credit market is showing a mixed but increasingly positive performance, the strategic cooperations with Banks are demonstrating clearly the benefits: private debt funds obtain preferred access to asset-based finance, direct lending and other private credit asset opportunities originated by a Bank.

Cross-border activity is increasing on the European private credit markets. A recent study found, that 90 per cent of surveyed professionals reported a growing number of cross-border direct lending deals in Europe, with the technology sector generating the strongest growth. The United Kingdom and Ireland – along with the Germany, Austria and Switzerland region – are spearheading this development.

2025: Outlook and market performance

Regulatory changes coupled with increased M&A activities are set to accelerate momentum on the 2025 private credit market. The increasing number of partnerships with banks will be of particular advantage to the non-sponsored direct lending segment, as they will open up new origination channels and mitigate the sourcing challenges that this strategy has often faced in the past.

This development opens up a strategic opportunity for German and European private credit managers – namely to significantly expand their deal pipeline while benefiting from the banks’ established client relationships. Regulatory developments ensure a sustainable structural transformation, changing private credit from a niche segment into a key component of corporate funding.

Contact

Contact  Downloads

Downloads  Newsletter

Newsletter