Newsletter

Newsletter In its most recent report, Listed Private Equity Insights, Invest Europe takes a close look at private equity managers or funds listed on stock exchanges around the world. Together with European Long-Term Investment Funds (ELTIFs), listed investors have played a vital role in democratising private markets, giving both institutional and private shareholders of all sizes direct access to one of the best-performing asset classes. As of year-end 2024, assets under management by listed private equity investors totalled more than 4.3 billion euros globally. With a combined market cap of over 550 billion euros, these firms made listed investors a key segment that is continuing to grow. Recent regulatory changes in the United States and compelling performance data from Europe have signalled a turning point for this share class. Traditional barriers between private and institutional investors are falling away.

Access for all investors

Listed private equity companies act as a bridge between the exclusive world of private markets and the broader investor base of public markets. Traditional private equity funds typically require investors to commit a certain minimum amount and undergo accreditation. In the case of listed private equity funds and companies, all that investors have to do is purchase a share. This model combines the flexibility, liquidity and regulatory oversight of public markets with exposure to high-quality private companies, which in many cases are not publicly traded.

Recent market movements are reinforcing the appeal of public access to private equity. While IPO activity in the US has slumped, assets under management in private markets have surged. At the same time, more private individuals are investing in the stock market. This mix has driven structural demand for access to private markets – which is being met by listed private equity companies.

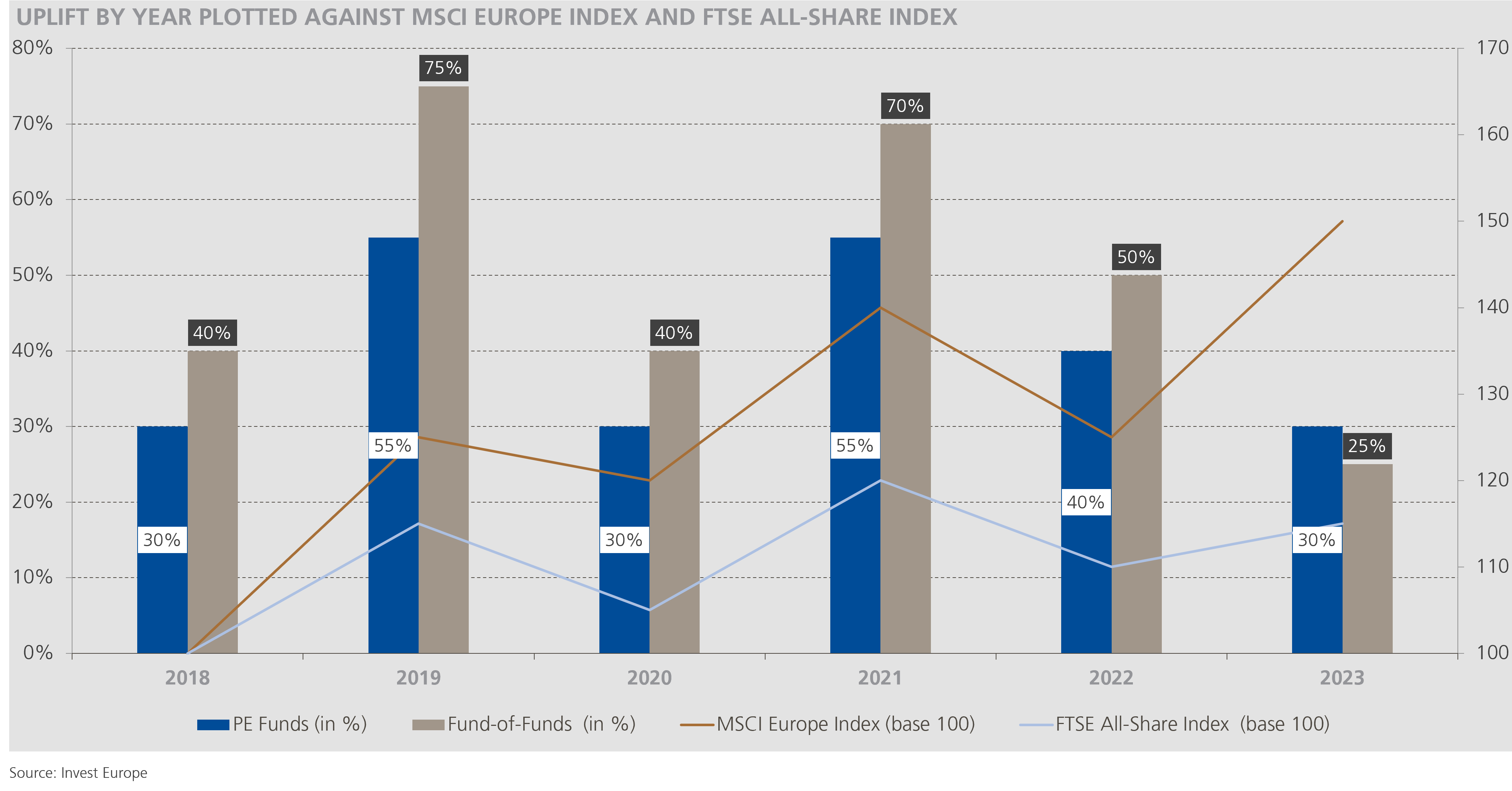

Validating conservative valuationsthrough exit performance

In recent years, listed private equity companies faced criticism mainly for the valuation of their portfolio companies. Invest Europe has now refuted these criticisms with an extensive analysis of 2,884 exit transactions conducted between 2019 and 2023. This data shows that listed private equity firms sold their portfolio companies at exit prices that were materially higher than the most recently reported carrying values.

Private equity funds generated a 39 per cent premium on exits compared with the most recent valuation, demonstrating that valuations are efficient and in line with markets. These precise valuations are the result of investors having direct access to portfolio companies and peer group companies. While it is true that funds of funds generate even higher premiums (49 per cent), this is mainly due to their structurally more conservative valuation approach, which reflects the complex diversification required when investing across multiple funds and vintage years. Such diversification increases risk and performance uncertainty, necessitating a more cautious valuation methodology.

Notably, even during the COVID-19 pandemic and the subsequent recovery, listed private equity exits delivered consistent premiums, underscoring the robustness of these valuation approaches.

Regulatory renaissance: SEC lifts investment barriers

2025 marked a pivotal shift in the regulatory landscape for listed private equity companies. The US Securities and Exchange Commission (SEC) reversed a position it had maintained since 2002, meaning that closed-end funds – which cannot issue any further shares after inception – are no longer required to limit their investments in private funds to 15 per cent of net assets. In a speech covering SEC innovations, Chairman Paul Atkins stated that, in the last ten years alone, private fund assets had almost tripled from 11.6 trillion US dollars to 30.9 trillion US dollars. He also pointed to more rigorous supervision as another factor contributing to the SEC decision.

For the very first time, this regulatory change allows closed-end funds to sell shares to both accredited and retail investors and without a minimum initial investment requirement of 25,000 US dollars. According to Division of Investment Management Director Natasha Greiner, the SEC hopes that this shift will provide investors with new investment opportunities that align with their risk tolerance and investment objectives.

Dynamic market growth despite persistent NAV discounts

Assets under management at listed private equity companies rose by an impressive 30 per cent in 2024, increasing from 3.3 to 4.3 billion euros. Market capitalisation climbed by 6.7 per cent to 552 million euros in the same year. This reflects not only growing interest among institutional investors but also the stronger performance of underlying assets.

In fact, listed private equity companies ranked among the stock market’s top performers in 2024. Emphasising the appeal of the underlying portfolio companies, the VanEck Global Listed Private Equity ETF returned approximately 44 per cent for the twelve months up to November 2024, significantly exceeding expectations. This strong performance stands in sharp contrast to the ongoing discount to NAV.

Job creation and macroeconomic impact

Listed private equity companies are driving job creation across Europe. In 2023 alone, 602 portfolio companies created more than 57,000 new jobs – averaging nearly 100 new jobs per company. In total, 890 portfolio companies now employ over 1.3 million people across sectors and regions.

These figures highlight the macroeconomic importance of listed private equity companies as engines of growth and innovation.

Structural trends and promising perspectives

On average, 22 per cent of institutional portfolios are invested in alternative assets. At the same time, institutional investors are continually increasing their allocation in private markets. Private equity, infrastructure, private credit and other alternative investments account for 15 per cent on average.

While the persistent NAV discount – even in the face of a strong performance – remains a challenge, it also presents opportunities for equity investors. As the authors of Invest Europe’s report point out, it is not the absolute NAV discount level but rather its change that drives future share price returns. This suggests that valuation metrics for listed private equity companies will need to adapt to a normalised interest rate environment.

Accessing private equity through technological innovation

Fintechs play a key role in further democratising private markets by developing solutions that enable fractional ownership of funds, which in turn broadens access to private market products. These technology-driven platforms lower entry barriers and allow investors across different asset levels to build capital through alternative investments.

The interplay of regulatory easing, technological innovation and performance has positioned listed private equity companies for continued sustainable growth. With a larger capital base, there are more funding opportunities for private companies and projects, potentially accelerating innovation and economic growth.

Structural changes with a sustainable outcome

The combination of impressive performance, regulatory easing and technological innovation paves the way for the long-term democratisation of private markets. With a proven track record and a robust regulatory framework, listed private equity companies offer investors of all sizes the chance to participate in the transformation and growth of private companies.

Structural changes in regulation, combined with a proven conservative approach to valuation and a strong influence on labour markets, make listed private equity companies a key component of any diversified portfolio.

Contact

Contact  Downloads

Downloads  Newsletter

Newsletter