Newsletter

Newsletter The private equity market has been showing clear signs of a sustainable recovery in 2025 so far, putting an end to a challenging period with low exit activity. This development provides a boost to the entire sector, as exit activity is not only a determining factor for investor returns but also releases fresh capital for new funds and has a favourable impact on the liquidity situation of fund investors.

Market revival supported by strong figures

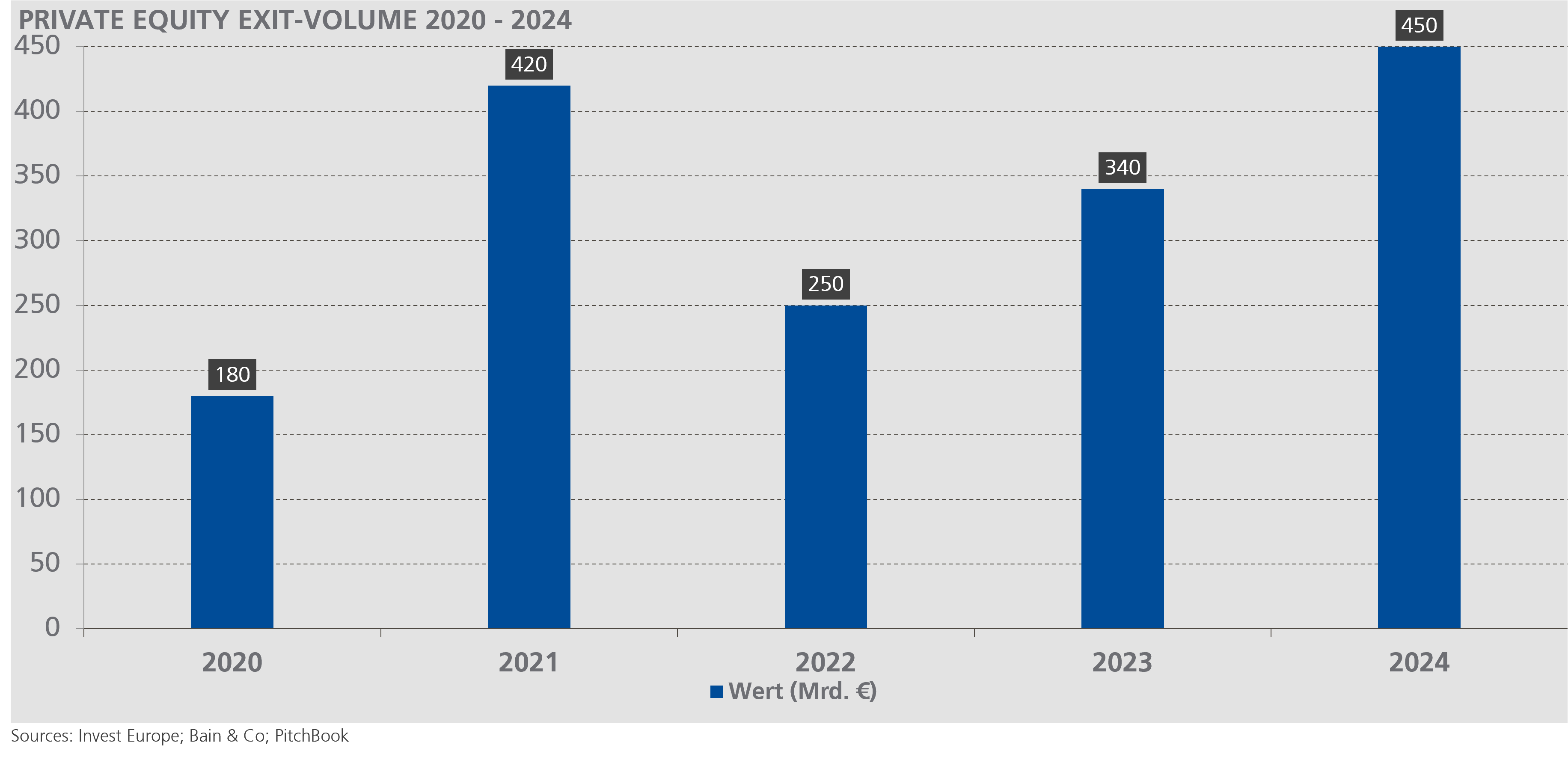

Global exit volumes rose by 34 per cent to 468 billion US dollars in 2024, while the absolute number increased by 22 per cent to 1,470 exits. North America and Europe in particular showed a strong year-on-year increase, whereas the situation on Asian market remained largely unchanged. The United Kingdom and Ireland spearheaded the European recovery with a 23 per cent increase in deals.

This positive development is in marked contrast to the challenges seen in recent years, when 57 per cent of private equity professionals delayed their exits due to inflation, high interest rates and/or geopolitical conflicts. Average deal sizes have also gone up: exits averaged 222 million US dollars in the fourth quarter of 2024, exceeding both the 2024 annual average of 186 million US dollars and the five-year average of 209 million US dollars.

Market dominated by secondaries

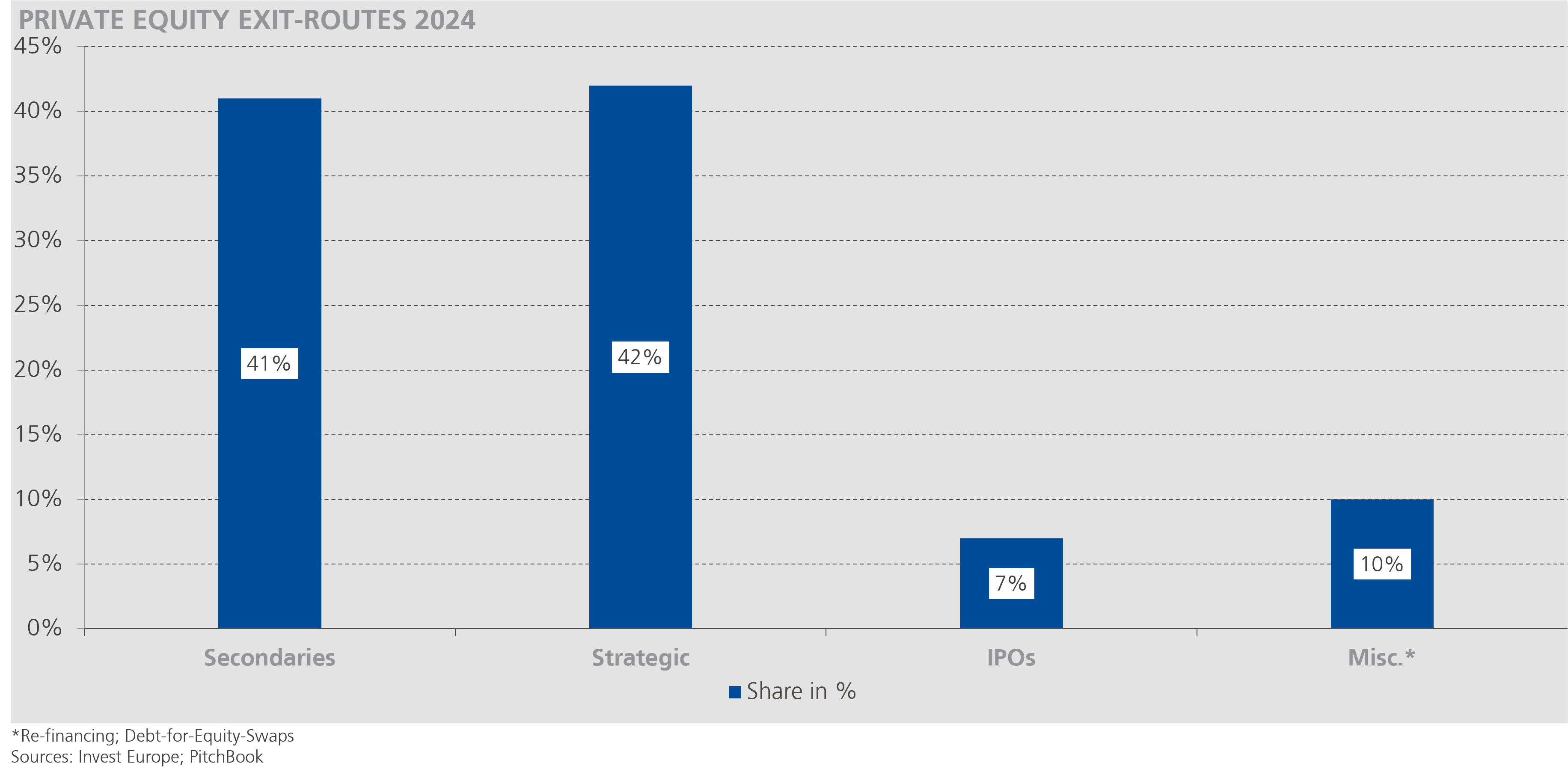

Market dynamics in the key exit channels brought about a remarkable shift over the 2024/2025 period. Secondary transactions, i.e. sales by financial investors to other financial investors, jumped by 141 per cent and made up six of the ten largest exits worldwide. This development shows that private equity firms are increasingly willing to invest in companies that offer further growth potential.

Sales to strategic buyers – i.e. to companies – remained largely stable year on year, but accounted for 82 per cent of the exit volume in the first quarter of 2025, compared with 59 per cent in the same period of the previous year. This shift indicates that strategic buyers are becoming more active and are willing to pay premium valuations for strategically valuable assets.

IPO market showing first signs of recovery

Activity on the IPO market is picking up again after a few very weak years. While IPOs accounted for only seven per cent of exits in 2024 in terms of value, the absolute number of IPOs soared from 158 in 2023 to 211 in 2024. IPO activities from companies with a financial investor generated approximately 7.9 billion US dollars in the first quarter of 2025, with six of the 14 deals making the top ten.

The solid IPO pipeline is sustained by the backlog of private equity exits and other IPO candidates. Experts are expecting IPO activity to pick up significantly in the first half of 2025 as the market environment continues to stabilise and the valuation gap between buyers and sellers narrows.

Developments on the European market

The European private equity market posted a strong recovery in 2024. Private equity and venture capital firms invested 126 billion euros – this was not only 24 per cent more than in 2023 but also far higher than the five-year average. Divestments rose by 45 per cent to 46 billion euros for a total of 3,517 companies sold – up 10 per cent on 2023.

The German market performed exceptionally well, with private equity divestments in 2024 amounting to around 3.3 billion euros. Consumer goods and services accounted for the largest share of the exit volume with about 40 per cent.

The exit market – driving factors for recovery

A number of different structural factors are driving the acceleration of exit activities expected in 2025. As portfolio holding periods are increasing – approximately 46 per cent of non-sold assets have been held for at least four years – financial investors are under considerable pressure to return capital to their fund investors. These extended holding periods, the longest of which date back to 2007, pose quite a challenge for financial and fund investors.

Recent interest rate cuts by major central banks have reduced financing costs, which in turn has had a stimulating effect on the deal market, including exits. Global dry powder reached record levels, amounting to 1.6 trillion US dollars at year-end 2024. Combined with the backlog of exits, this large volume of non-invested capital is set to boost both supply and demand on the M&A market in 2025.

Alternative liquidity solutions on the rise

Innovative liquidity solutions are also continuing to evolve alongside traditional exit activity. For instance, continuation funds are becoming increasingly popular, especially for “trophy” assets. These investment vehicles allow financial investors to hold successful portfolio companies for a longer period of time, while offering their fund investors a choice between capital returns and a stake.

Outlook for 2025 and beyond

The outlook for 2025 is optimistic. Experts expect exit activity to accelerate, with the strongest momentum coming in the second half of the year. The European M&A markets are already on the path of recovery, as the United Kingdom and the Germany, Austria and Switzerland region continue to dominate PE activity.

Technology and healthcare are the sectors with the most promising growth outlook, with the individual sub-sectors performing differently within each sector. Strategic US buyers remain important players on the market and account for around one-third of strategic purchasing activity in European PE exits.

Record dry powder levels, extended portfolio holding periods, improved financing conditions and an increasingly cooperative regulatory environment all combine to pave the way for a sustainable recovery of the exit market. And even though short-time volatility and geopolitical uncertainty continue to pose a challenge, structural drivers indicate that the private equity exit market will recover in the coming years.

Contact

Contact  Downloads

Downloads  Newsletter

Newsletter